A credit score is one of the important loan requirements. All lenders check the credit score of the borrower before approving a loan. This makes goes without saying that a high credit score is a crucial loan eligibility criteria. In this blog, we shall discuss what credit score is, how impacts it, how to check credit score, and how to improve credit score.

Table of Contents

What is a Credit Score?

Also Read: How to get a Business Loan?

A credit score is also called a CIBIL score. It is a 3-digit number that represents an individual’s creditworthiness. A credit score depicts the financial behavior of an individual. And so, before approving or sanctioning a credit, lenders check CIBIL score of the borrower to ensure they are lending their money to the right borrower.

This score is a sum of the bank statement, loan repayment history, number of debts availed, and credit card history. Notably, a high credit score signifies that the individual is credible and can be trusted with money. So, lenders only offer and sanction loans to people with high CIBIL score.

What is a Good Credit Score?

Also Read: How to Manage Working Capital for Small Business?

A credit score lies between 300 and 900. The best CIBIL score is termed as the one which is near 900. Most of the lenders offer loans to individuals who have a score of more than 900. So, a minimum CIBIL score for a loan is 700. Notably, a high CIBIL score signifies less risk for the borrower. And therefore, they offer loans at a low interest rate to borrowers with high CIBIL score.

What Impacts Credit Score?

Also Read: When to Apply for a Loan for Business?

A high CIBIL score is important not just for the loan to get approved but also at the lowest interest rate. Following are the factors that affect credit score:

Payment History

The payment history of the borrower signifies if he is trustable with money or not. Said that, if the borrower pays all his time, it impacts the CIBIL score positively. There is a section in the credit report for payment history. This section provides information such as bank details, timely payment of the loans, number of loans and debts availed in the past, and the number of cheques bouncing and EMI defaulting instances (if any).

Current Debts & Running Loans

Running debts and current loans also impact the credit report. If the borrower is running on a number of debts and loans, this signifies the borrower’s credit hungry behavior. This represents that the borrower is in habit of living in debts. In addition, if the borrower applies for many loans in a short period of time and they get rejected, this negatively impacts the credit report.

Credit History

The credit history of the borrower represents his loan repayment habit. Every lender wants his money to be repaid on time and therefore, they ascertain their repayment history. If the borrower has defaulted on any EMI or his cheque is bounced, this is most likely to impact negatively on the credit score.

Credit Utilization Ratio

Credit utilization ratio is the amount of credit that the borrower uses every month. If the borrower uses his credit card to its entire limit, this signifies that he is habitual of living on debts. This again impacts negatively on the credit report and brings the score down.

How to Check Credit Score?

Also Read: How to Check Business Loan Eligibility Criteria in 30 Seconds?

TransUnion is CIBIL is the company that tracks and records an individual’s loan and financial history. To check CIBIL score, follow the following steps:

- Initiate the process of CIBIL on TransUnion’s official website.

- Enter personal details.

- Pay the fees.

- The report would be emailed to your mail account.

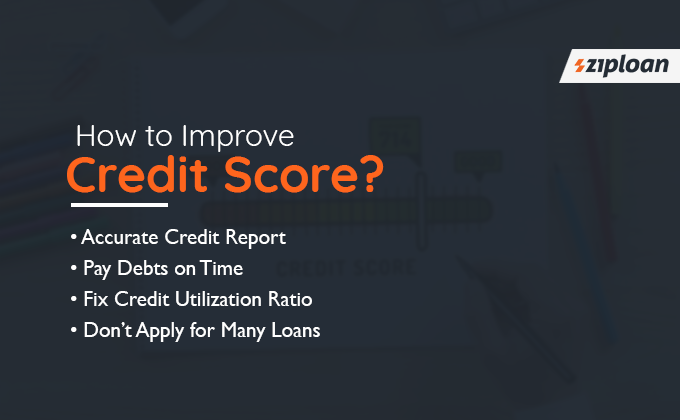

How to Improve Credit Score?

Also Read: Business Loan EMI Calculator: How to Calculate EMI Online in a Minute?

Follow the following steps to improve your CIBIL score:

Accurate Credit Report

The borrower must check his credit report from time to time. And in case any wrong information is entered in the report, he can get it rectified by the CIBIL. This is an important point since there are times when wrong information is entered in the CIBIL. And any such wrong information can bring the CIBIL score down.

Pay Debts on Time

It is important to pay all the debts on time. The timely payment of debts depicts the borrower’s responsible behavior and impacts positively on the score. In addition, it is suggested that the borrower must not wait for the due date and pay his bills at least 5 days before.

Fix Credit Utilization Ratio

As suggested before, the borrower must not spend the entire limit of the credit card. And if he is spending the limit, he should immediately fix it. The ideal credit utilization limit is 30%-40% of the sanctioned credit card limit.

Don’t Apply for Many Loans

Applying for many loans in a short period of time shows credit hungry behavior of the borrower. And this reflects on the credit report as well. So, in case the borrower’s loan application is rejected, he should apply for next loan after at least three months. It is worth mentioning that the borrower must only apply for a loan after knowing the eligibility criteria and document requirements. And apply for a loan only if he meets them.

Want to read the latest posts on social media? Then follow us on Facebook, Twitter, and LinkedIn!